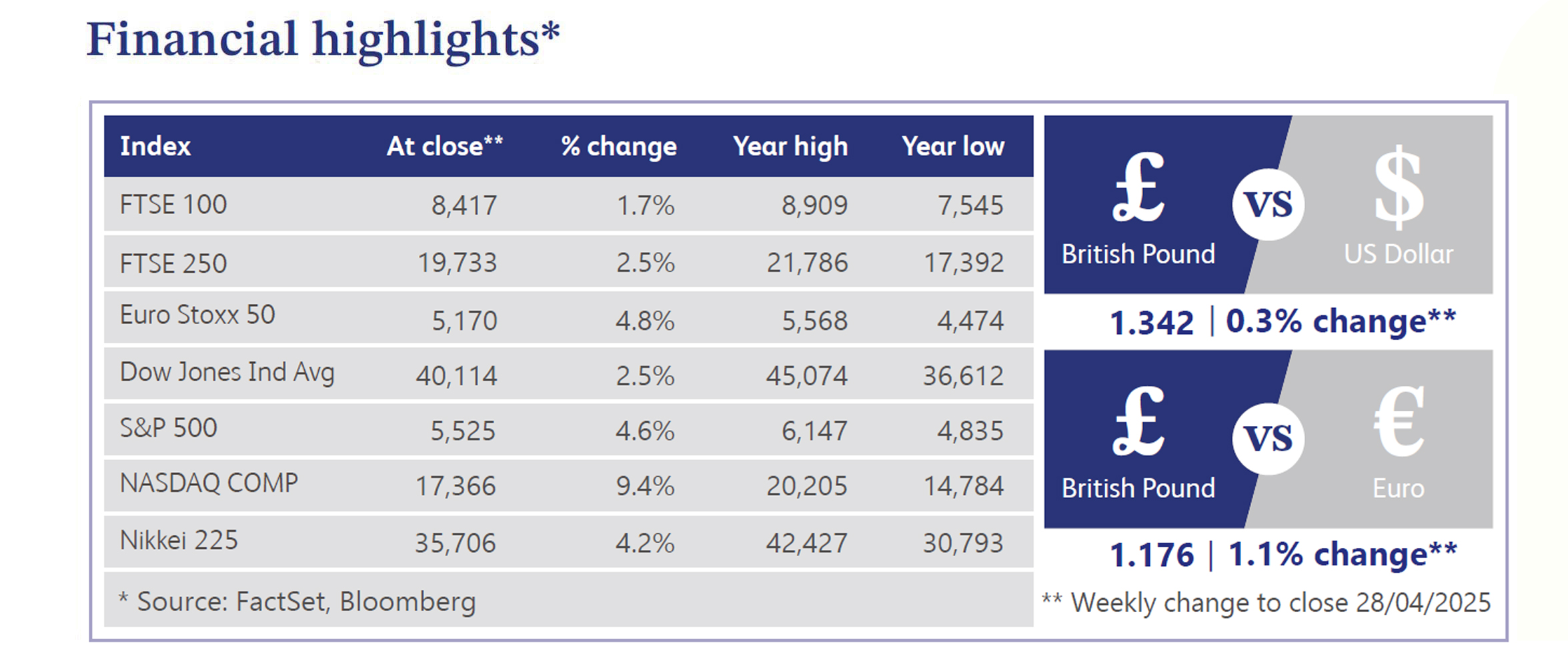

29 April 2025

UK economic sentiment weakened sharply last week as global trade tensions intensified. The International Monetary Fund (“IMF”) cut the UK’s 2025 growth outlook to 1.1%, the steepest downgrade among major European economies, but noted the UK may still outpace its G7 peers. Economic activity slowed sharply, with the composite Purchasing Managers' Index (“PMI”) falling to a 29-month low of 48.2, signalling a contraction. Consumer confidence deteriorated amid rising cost pressures, though retail sales surprised on the upside. Business leaders voiced concern over red tape costs and the threat of tariffs, warning of imminent job losses unless a US trade deal is struck. However, a KPMG survey found financial services leaders remain optimistic about London's prospects, planning significant investments despite global uncertainties. The Bank of England (“BoE”) indicated it would weigh the impact of trade shocks at its May meeting, with rate cuts still in play. Overall, markets faced mounting signs of economic stress alongside cautious policymaker rhetoric.

UK Chancellor Rachel Reeves reiterated that the Autumn Budget will not include wealth tax increases or changes to capital gains tax (“CGT”), aiming to protect fiscal discipline while supporting growth. However, fiscal drag - caused by frozen tax thresholds - is set to impact an additional 8.3 million people by 2029-30, according to the Office for Budget Responsibility (“OBR”). In trade talks, Reeves indicated readiness to cut tariffs on US cars and agricultural products to secure a US deal but ruled out lowering food standards. Ahead of a key meeting with US Treasury Secretary Scott Bessent, Reeves stressed that improving UK-EU trade ties remains a bigger priority for long-term growth. UK-EU negotiations on defence, fishing and youth mobility are moving closer to unlocking a broader economic agreement. Political tensions also rose, with calls for a Conservative–Reform UK alliance ahead of the next election.

US equities rallied, with the S&P 500 and Nasdaq posting their second-best weeks of 2025. High-beta stocks outperformed defensives, led by big tech gains, with Tesla up 18.1% and Nvidia up 9.4%. Semiconductors, metals, credit cards, investment banks and casinos also strengthened, while telecoms, consumer staples, managed care and energy lagged. Trade tensions with China eased after the White House signalled tariff reductions and new deals with Japan and India. Federal Reserve (“Fed”) independence concerns faded after Trump softened his stance on Chair Jerome Powell. Treasury yields fell slightly with the yield curve flattening; the US Dollar Index rose marginally; gold declined and Bitcoin futures surged 11.7%. Macro data was mixed, with weaker PMIs but stronger home sales. Strategists turned cautious, with Deutsche Bank and Jefferies cutting their S&P 500 targets, citing weak earnings momentum outside megacap tech, although first-quarter earnings per share (“EPS”) growth improved and margin risks from tariffs and a weaker dollar were flagged.

Mortgage completions in the UK surged by 50% in March, marking the biggest monthly increase in over three years, according to Barclays data reported by The Times. The jump was driven by buyers rushing to complete transactions ahead of the 1st April stamp duty threshold changes. First-time buyers led the surge, with completions up 70% compared to February. The sharp rise reflects the impact of policy changes on housing market activity, with many seeking to lock in lower tax rates before the new rules came into effect.

Antofagasta, the Chilean-based copper mining and transport group, saw shares rise 10.4% after RBC Capital Markets upgraded its rating to Sector Perform, citing a "more comfortable" risk profile amid copper price volatility. Analysts highlighted resilient Chinese demand offsetting trade war risks and noted the company's strong balance sheet, despite peak capital expenditures at Los Pelambres and Centinela. Although RBC trimmed the price target due to foreign exchange adjustments, other industry analysts raised theirs, seeing opportunity in the recent sell-off. Improved 2025 EPS forecasts further boosted sentiment, helping Antofagasta outperform despite broader concerns about lasting economic damage from trade uncertainties.

Croda International, a specialty chemicals manufacturer, surged 9.6% after reporting 8% year-on-year first quarter group sales growth to £442 million, surpassing Jefferies' estimate of £417 million. The company reaffirmed its Fiscal 2025 profit before tax (“PBT”) outlook of £265 - 295 million and announced a tariff surcharge strategy to offset potential US trade tariffs. Investor sentiment was also buoyed by broader market optimism after US comments signalled trade de-escalation with China. Croda’s better-than-expected sales and stable profit guidance positioned it as the FTSE 100’s top performer, reflecting strong confidence in its resilience amid external pressures.

Marks & Spencer Group, the British retail giant, fell 6.2% after revealing it had been managing a cyber incident that forced temporary operational changes. Although stores, websites and apps remained functional, the announcement of paused online orders and the engagement of external cybersecurity experts raised investor concerns about potential reputational and financial impacts. M&S reported the incident to regulatory authorities, but the lack of detailed disclosure about the breach's nature and extent fuelled market nervousness. The cyber event overshadowed broader positive market sentiment, weighing heavily on M&S shares amid heightened scrutiny over cybersecurity resilience.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.