7 July 2026

Last week, Bank of England Governor Andrew Bailey downplayed the possibility of rate cuts this year, noting the central bank is comfortable leaving interest rates on hold. While inflation is expected to return to its 2% target later than preferred, markets have already tightened the bond yield curve. Soaring energy costs remain a concern, with upcoming price cap increases threatening to push millions of households into fuel poverty. Consequently, officials are maintaining a cautious stance, especially as Bank of England Monetary Policy Committee member policymaker Catherine Mann signalled a readiness to hike rates if price pressures persist. Meanwhile, domestic food price inflation hit a multi-month low as retail competition and promotional activity helped keep shop prices in check.

In equities, the FTSE 100 index finished the week up, buoyed by Middle Eastern ceasefire progress, which has begun to ease the extreme inflationary pressure on the domestic economy. However, UK government bond markets face new scrutiny as the central bank plans to limit debt levels for hedge funds, reflecting broader concerns over fiscal stability. This fiscal policy environment remains under immense pressure as incoming leadership must address a massive defence funding gap, highlighted by the ongoing geopolitical tensions, alongside looming capital spending cuts. While Treasury officials expect the Middle East conflict to have a limited long-term impact on public finances, markets are now anticipating potential tax increases to bridge the deficit. This transition comes as the official process to select a new Prime Minister gets underway this week, following Sir Keir Starmer's resignation last month, with favourite replacement Andy Burnham expected to outline a more detailed economic agenda shortly.

Across the Atlantic, macroeconomic data heavily impacted market sentiment as June non-farm payrolls arrived weaker than forecast, only adding 57,000 vs the expected 115,000. This reinforces a resilient economic growth narrative despite falling labour force participation. In equities, major United States indices were mostly higher even while closing a day early to observe the 4th of July bank holiday on Friday. The Nasdaq Composite index emerged as the standout performer. Technology stocks lifted the market periodically, driven by strong momentum in artificial intelligence and big technology companies, though some rotation into other sectors occurred midweek amid profit-taking. United States Treasury prices weakened with yields rising across the curve, following a hawkish shift in Federal Reserve expectations as markets reduced the likelihood of a July rate hike in favour of sustained higher levels. Meanwhile, the US Dollar weakened as gold prices rose. Geopolitical developments firmly took a backseat as the macro focus shifted back towards the labour market. The clearer path towards a resolution which reopens the Strait of Hormuz has significantly calmed energy markets, allowing flows to recover faster than expected. This optimism pushed West Texas Intermediate crude oil down noticeably, settling lower for the week at pre-war levels.

Finally, UK house prices recorded a flat performance, with the mortgage lender Nationwide reporting stagnant monthly figures, as rising energy prices dented momentum. However, weak consumer confidence, keeping prospective home buyers increasingly cautious, is further increasing the pressure.

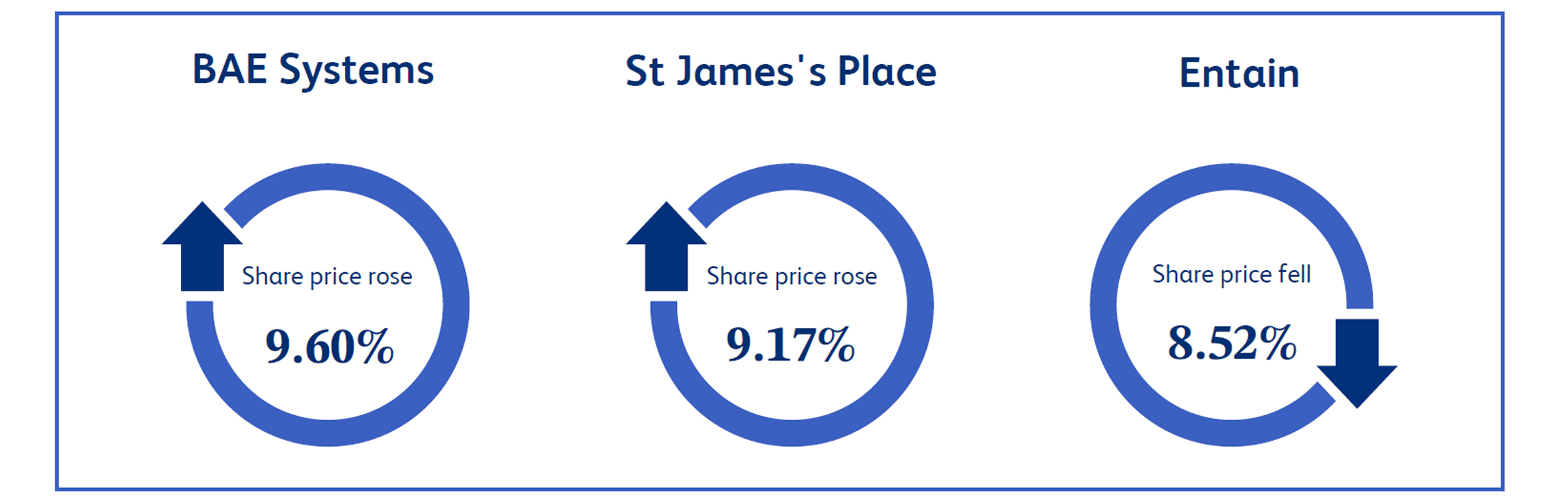

BAE Systems, the leading multinational defence, security and aerospace company, saw its shares rise 9.60% last week. This positive movement in the share price was driven by significant corporate and national developments, notably the announcement of a massive contract awarded by the Ministry of Defence to its joint venture to support the next development stage of the Global Combat Air Programme advanced fighter jet. Investor enthusiasm was further bolstered by the UK government's commitment to a £15 billion expansion in military spending to address the evolving global security landscape.

St James's Place (“SJP”), the largest UK wealth manager, saw its shares rise 9.17% last week. This gain was boosted after the wealth manager announced plans to expand its wealth solutions in Asia and the Middle East. At the same time, analysts raised their price target, noting SJP's market share gains should help offset ongoing AI-disruption fears weighing on parts of the sector. The upgrade highlights that SJP continues to extend its leading position in the UK wealth market, underpinned by its adviser Academy. The stock has also benefited from a broader rotation into previously beaten-down UK names.

Entain, the global sports betting and gaming group with major brands such as Ladbrokes and Coral, watched its shares drop by 8.52% last week. This steep decline was largely triggered by market anxieties following a confirmed massive increase in UK Gambling Commission licence fees, alongside the issuing of new equity under its internal savings plan. Since these regulatory hurdles squeeze domestic margins, the market braced for a tougher operating environment, which heavily overshadowed previous momentum gained from the recent disposal of its Central and Eastern European business to trim debt.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.