31 March 2026

Last week, the UK economy experienced high macroeconomic volatility as stagflation fears intensified after the Iran conflict disrupted global supply chains. March’s Purchasing Managers' Index (PMI) fell to a six-month low, while consumer expectations also dropped as households faced increases in energy prices. Initial panic over Bank of England (BoE) rate hikes, driven by the energy crisis, faded as BoE officials dampened inflation fears. They argued that the domestic economy lacks the momentum to sustain a 2022-style price spiral where costs drove wages and prices higher. Downing Street remains in active crisis management; Prime Minister Starmer is set to meet business leaders to navigate the fallout and discuss how the government and private sector can collaborate. Chancellor Reeves is attempting to avoid Truss-era panic by delaying unfunded universal bailouts, with broad energy support postponed until at least the autumn.

Britain’s defensive posture is becoming more evident in the conflict in the Middle East. Recently, the UK authorised US strikes from the Diego Garcia base and is now moving to intercept Russian shadow fleets. However, following strong public pressure from US President Trump, Starmer remains adamant that the UK will not be dragged directly into the war. Despite the volatility, Starmer is pushing for a trade reset, preparing government legislation to reinstate certain EU directives to ease post-Brexit friction.

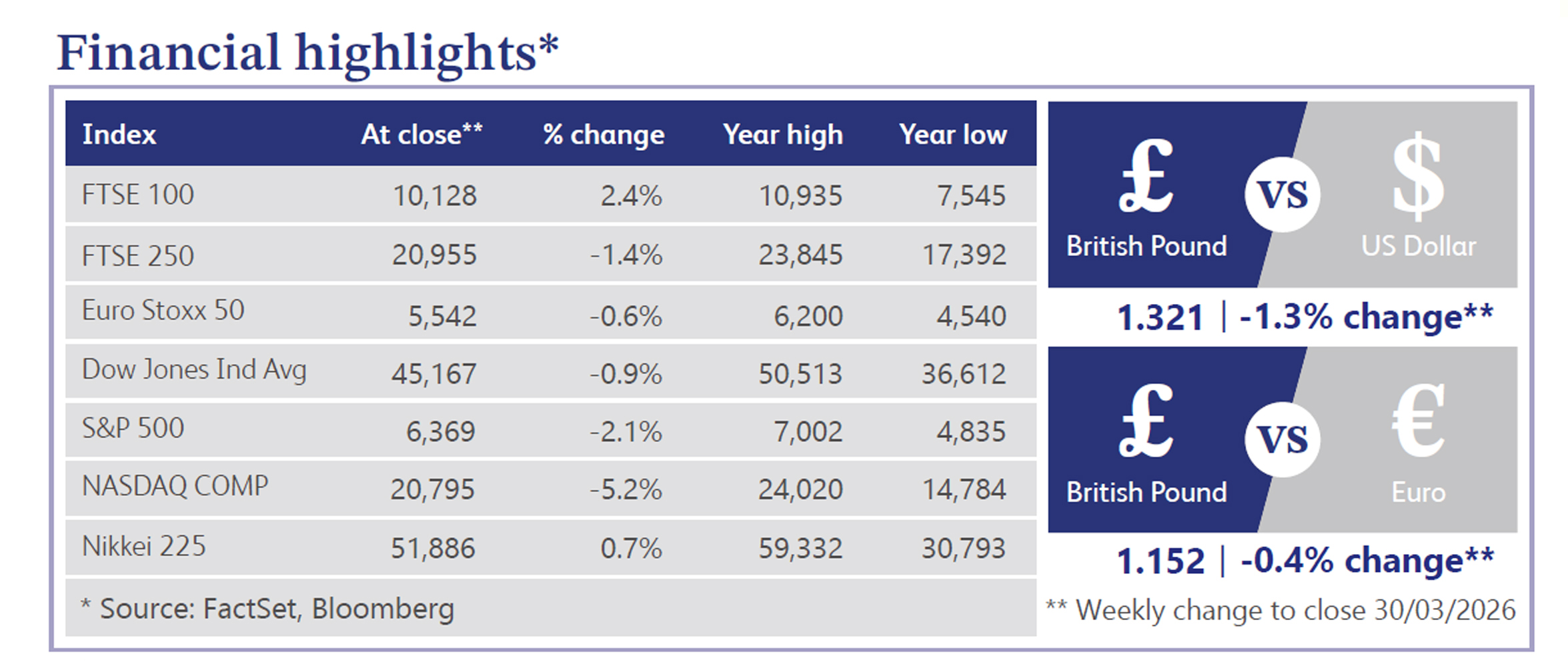

This geopolitical tension has shaken the markets, though early-week panic eventually gave way to a relief rally. Britain’s energy crisis triggered a reprice, pushing the 10-year Gilt yield to an 18-year high as markets initially priced in four BoE hikes. As BoE officials dampened these fears and pushed back against the narrative, expectations fell to two hikes. This remains a stark contrast to pre-war forecasts, where rate cuts were seen as near-certain. Equities rebounded on de-escalation hopes, with energy and mining names leading the recovery on the back of easing interest rate fears. However, retailers warned of impending price increases, highlighting ongoing margin pressures.

Across the pond, the S&P 500 registered its fifth consecutive loss, and the Nasdaq slipped into correction territory. The sell-off saw a decline in big tech, software, and memory stocks, while the Russell 2000 gained. A record hedge fund sell-off occurred as energy and commodity-linked stocks outperformed and oil surged. The Iran conflict continues to dominate market sentiment. President Trump announced a pause in strikes for peace negotiations, but the involvement of Houthi forces, threats to uranium facilities, and the deployment of additional troops by the Pentagon have left investors on edge. This instigated a bond market sell-off, driven by weak Treasury auctions and stagflation concerns following U.S. March PMI data. Despite the geopolitical gloom, corporate earnings remain a bright spot as analysts continue to upgrade profit targets.

The UK housing market faces increasing headwinds, despite mortgage approvals in February and house price inflation being quite resilient. BoE's rate outlook shift has impacted affordability massively. Geopolitical instability and rising swap rates, has led to lenders withdrawing roughly a fifth of available mortgage products and average two-year fixed rates have increased, driving a notable year-over-year decline in active buyers as uncertainty deters demand.

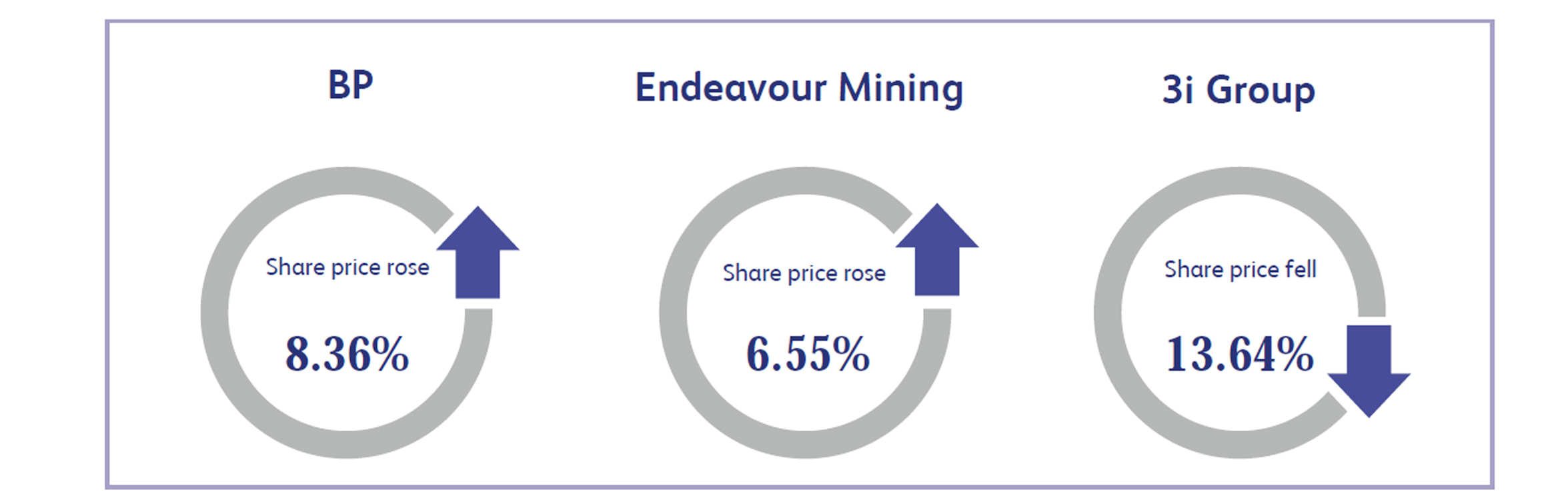

BP, a major European energy company operating in global oil production and refining, surged 8.36% this week. Shares initially fell at the start of the week, after President Trump paused strikes on Iranian infrastructure, but quickly rebounded as geopolitical risk premiums re-entered the energy market. Supported by high oil prices, analysts have turned broadly positive on the sector, as strong macroeconomic tailwinds allowed the stock to power through company-specific challenges. Notably, the market largely shrugged off BP's recent suspension of its share buyback programme and an ongoing labour workforce lockout involving nearly 1,000 union workers at its Indiana refinery, focusing instead on the broader commodity rally.

Endeavour Mining, a precious metals miner operating within the broader global commodities extraction sector, rose 6.55% this week. The rally was fuelled by increasing optimism over the possibility of de-escalating the conflict in the Middle East. The positive prospects of imminent meetings between the US and Iranian governments alleviated investor concerns over the threat of a renewed, conflict-driven inflation spike. As these headwinds temporarily eased, investors confidently rotated back into precious metal equities, providing a strong lift to Endeavour alongside its sector peers.

3i Group, one of the largest private equity funds with an international portfolio of investments, recorded a sharp fall of 13.64% this week. The sell-off was driven entirely by Action, the European discount retail chain that accounts for roughly 70% of the fund’s net asset value. Action announced plans to undertake a highly ambitious, but risky, operational expansion into the US market. Although the retailer reported impressive projected net sales of €16 billion for 2025, investors were highly apprehensive about 3i's severe concentration risk and the historical difficulties European retailers face when attempting to crack the US market. Furthermore, analysts warned that sticky inflation, exacerbated by the Middle East conflict, will likely disproportionately squeeze the disposable income of the discount retailer’s core demographic.

Market Commentary prepared by Walker Crips Investment Management Limited.

This publication is intended to be Walker Crips Investment Management's own commentary on markets. It is not investment research and should not be construed as an offer or solicitation to buy, sell or trade in any of the investments, sectors or asset classes mentioned. The value of any investment and the income arising from it is not guaranteed and can fall as well as rise, so that you may not get back the amount you originally invested. Past performance is not a reliable indicator of future results. Movements in exchange rates can have an adverse effect on the value, price or income of any non-sterling denominated investment. Nothing in this document constitutes advice to undertake a transaction, and if you require professional advice you should contact your financial adviser or your usual contact at Walker Crips. Walker Crips Investment Management Limited is authorised and regulated by the Financial Conduct Authority (FRN:226344) and is a member of the London Stock Exchange. Registered office: 128 Queen Victoria Street, London, EC4V 4BJ. Registered in England and Wales number 4774117.

Important Note

No news or research content is a recommendation to deal. It is important to remember that the value of investments and the income from them can go down as well as up, so you could get back less than you invest. If you have any doubts about the suitability of any investment for your circumstances, you should contact your financial advisor.

The value of investments can fall as well as rise. Investors may get back less than invested. Past performance is not a reliable indicator of future results.

The value of investments can fall as well as rise. Investors may get back less than invested.